Attention SPAMMERS: Don't advertise your services on my blog. If you do then you will have implicitly given me permission to disable any service you advertise via my blog by any means necessary.

“You provide the money and know-how to grow the business and I’ll provide the technology.”

My Bank Bashing Article

And then there’s that (draft) bank bashing article I wrote and hesitate to publish.

It expresses frustration with our current banking system.

Here’re a few lines from that article:

Why do we accept bank fees as a given?

Why do banks get to hold on to my money for 7 days? Why do banks get to earn interest on that money of mine, charging me NSF fees even though I have plenty of money.

Why is it okay for our deposits to be “processed” only during “business work days”?

Do banks use only bank employees, i.e., humans, that don’t work weekends and frequently take vacations to process our transactions?

No. Of course not.

Right Wing Extremism

Let’s not forget my How Does the Central Bank Print Money? article.

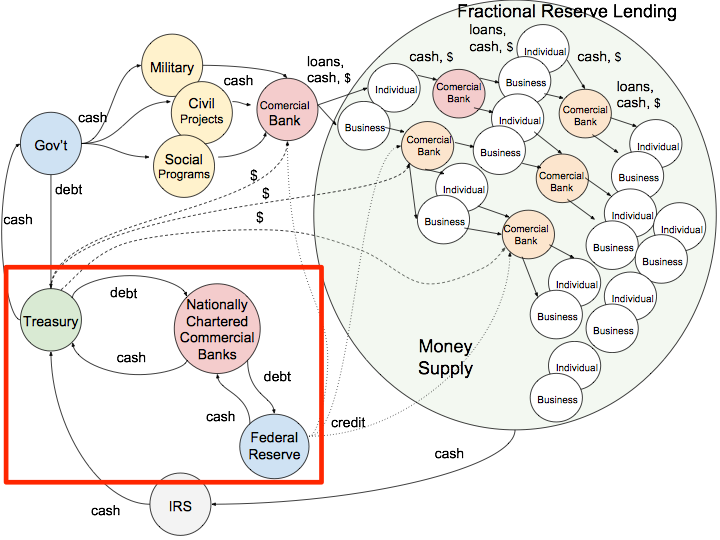

I returned to the diagram I created in that article and added a few more details. Let’s focus on that now (the red box below):

The nationally charted commercial banks are special banks that are given the privilege of buying bonds (Treasury Bills) at a low price and selling them to the Federal Reserve (the Central Bank) for a profit.

These elite banks buy low and sell high.

These elite banks serve the same purpose as Bitcoin miners. When they sell the bonds to the Fed, the money that appears on their electronic balance sheet is new money. That is where our USD money is actually minted.

The physical dollars and coins “minted” by the Treasury (the “$” in the diagram) closely reflect that newly minted money.

These elite banks are like Bitcoin miners, but instead of solving a cryptographic puzzle to get rewarded with Bitcoins all these elite banks have to do is give the Fed the T-bills that they got from the Treasury. It’s all done electronically. (If there were such a thing as the Illuminati, this would be it!)

Left Wing Extremism

This sums up what happened in our 2007–2008 financial crisis:

Acorn => Banks => Bad Loans => Financial Crisis

Fannie/Freddie => Bad Loans => Financial Crisis

Wall Street *** => Bad Loans => Financial Crisis

The Association of Community Organizations for Reform Now (Acorn) sued and extorted banks which into making bad loans, in an effort to put lower income citizens into houses that they could not afford.

Fannie Mae and Freddie Mac were created by Congress to provide low cost loans. They made a lot of very bad loans, i.e., they allowed low income people to move into high rent homes that they could not afford.

Lobbyists and political action committees and nonprofit organizations exerted influence over members of the U.S. Congress to ensure that Fannie/Freddie were allowed to continue to grow and take on unreasonable risk under their congressional charters and implied federal backing.

The U.S. Congress gave Wall Street firms (AIG, Citi, Merrill Lynch, RBS, UBS, JPM) the ability to compete — Wall Street firms had been complaining about the unfair competition from Fannie/Freddie — by permitting them to package bad loans and sell them to investors.

*** Granted “Wall Street” is considered more right-wing than left-wing, but there’s more left-wing non-sense in this section than the other.

Fractional Reserve Lending

See the big green circle in the diagram?

That’s where Alice deposits $100 in bank 1 that takes Alice’s money and loans out $90 to Bob.

Bob puts his $90 in bank 2 that takes Bob’s money and lends out $81 of it to Cindy, etc.

This process drastically increases the money supply in circulation.

It’s great; however, it only works when the banks make good loans.

The financial crisis of 2007–2008 is an example of what happens then banks make bad loans. The whole system implodes.

It’s not fair, but it’s real

Is it fair that some loud mouth special interest group can extort banks into making bad loans?

Is it fair that banks can still make money even when they make bad loans?

Is it fair that special interest groups can lobbied congress to allow Fannie Mae and Freddie Mac to make bad loans that almost bankrupted our economy?

Is it fair that congress would allow Wall Street firms to knowingly package bad loans and sell them to citizens as “good” investments?

Is it fair that all these shenanigans were permitted, that nearly threw us all into the next Great Depression and yet nobody went to jail?

Who was held accountable for playing politics with our financial security?

Wall Street firms got bailed out.

Wall Street executives got golden parachutes.

Banks still make money coming and going no matter how bad they screw up.

That frustration created the motivation that created Bitcoin.

Bitcoin was born

On November 1, 2008, a post appeared on a discussion forum called the Cryptography Mailing List …

“Abstract. A purely peer-to-peer version of electronic cash would allow online payments to be sent directly from one party to another without the burdens of going through a financial institution.”

… and was signed with the pseudonym Satoshi Nakamoto.

Many other attempts at digital currencies had all failed.

Then, two months later on 3 Jan 2009 Satoshi mined the first 50 bitcoins (known as the Genesis block).

Encoded in that Genesis block are the words:

“Chancellor on brink of second bailout for banks”

… that suggests that Satoshi frowned upon the bank bailouts of 2008. He wasn’t just a coder; his motivation was political.

I thought it was just what the market needed…

Now, back to my thoughts on the Lightning Network (LN) ...

The more models I created to simulate the workings of the LN, the more it became apparent that well funded hubs would be required to make the payment channels work as a general purpose point of sale system.

Where would the well funded hubs come from? Who has tons of money?

Banks.

Shit!

When that happens, we’ll be back where we started only this time around there will be no customer service, no branch offices, nobody to call to handle fraud, reverse bogus payments, etc. (Or maybe the banks will create “new” cryptocurrency customer support services for the LN side chains.)

The banks will still be the middlemen, charging whatever fees they see fit.

What Happened to Bitcoin?

Satoshi Nakamoto intended to build a decentralized cryptocurrency; a currency that would be free from political lobbyists, the U.S. Congress and unscrupulous Wall Street firms.

Most people think Bitcoin is free from centralized control; that’s not true.

Bitcoin’s source code is now largely controlled by single private company.

They have the power to change the rules of how Bitcoin works.

For example, they could increase the blocksize, therefore increasing the scalability of Bitcoin, but they have kept it at 1MB.

This plays right into their business plan, i.e., to make money on side chain networks, like the Lightning Network.

This bothered me for a while.

Cryptocurrencies are like Apps

Then, I heard Andreas Antonopoulos talk about cryptocurrency sovereignty.

Consider this use case that includes multiple internet-aware apps:

You read a Twitter tweet that makes you think Alice.

You start chatting with Alice over Telegram.

Typing becomes too much so you request a Google Hangout in order to talk.

You switch to video when you realize Alice has something on the white board to share.

You begin recording and save the .mp4 file.

You followup with an email summary of your meeting, including a link to the .mp4 video file.

You just used 4 different applications to communicate

Maybe cryptocurrencies will be like that. We’ll use multiple cryptocurrencies to transact business.

We may use one for a quick payment to a friend, another to pay a mortgage payment and yet another to buy that toy that we don’t want anyone else to know about.

Multiple cryptocurrencies for multiple purposes.

Enjoy paying fees for the customer support services? Use crypto A.

Dealing with friends and want super low fees? Use crypto B.

Prefer privacy? Use crypt C.

Who is going to create that killer cryptocurrency wallet app that makes such transactions quick, easy and affordable?

Ah, now I feel better. Time to go to sleep.

Nite nite.

Gaining Understanding and Confidence

It’s easy to get tripped up with questions about how the US monetary system works.

Throw cryptocurrencies into the equation and it can get overwhelming.

I grew up with a mom that was intrigued with US economy, currency, gold and other investments.

I guess that’s why cryptocurrency (and blockchain technology) is so interesting to me.

I get to combine the rhetoric that I heard in my formative years with my education and professional experience.

I invested my time, energy and resources to develop a training course to help others “get it”.

The first class is all about money (what it is, its history and relationship to digital currencies) and would serve as a good educational resource for those in finance and insurance professions.

The rest of the course is about how to leverage our understanding of money and blockchain technologies to build our own cryptocurrency.

Join me in class where we’ll:

Distill facts from fiction

Provide pertinent resources on a guided journey of learning

Provide well structured lab assignments

Provide starter projects (and completed solutions)

Provide insightful visual presentations

Provide a Certificate of Completion to attendees that finish the assignments

… and that’s just the 1st half of the course. In the 2nd half we cover the Ethereum blockchain.

I have condensed this class into an Immersive one week Master Class in Atlanta, GA.

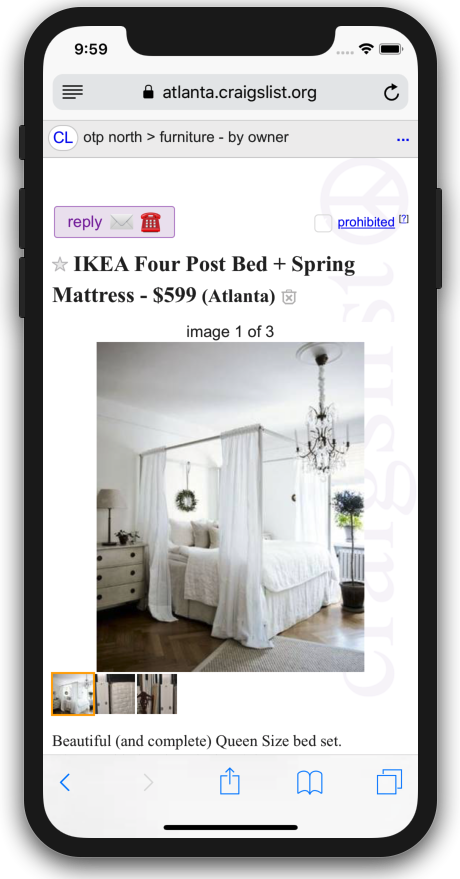

This is a story about my experience selling my furniture on craigslist.

My daughters graduated high school and left home for college. I decided to sell their used furniture.

First, I posted this ad on craigslist:

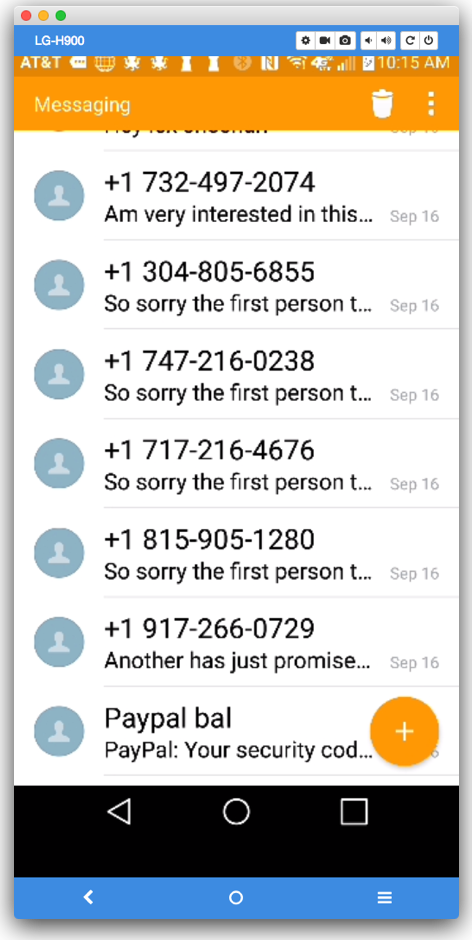

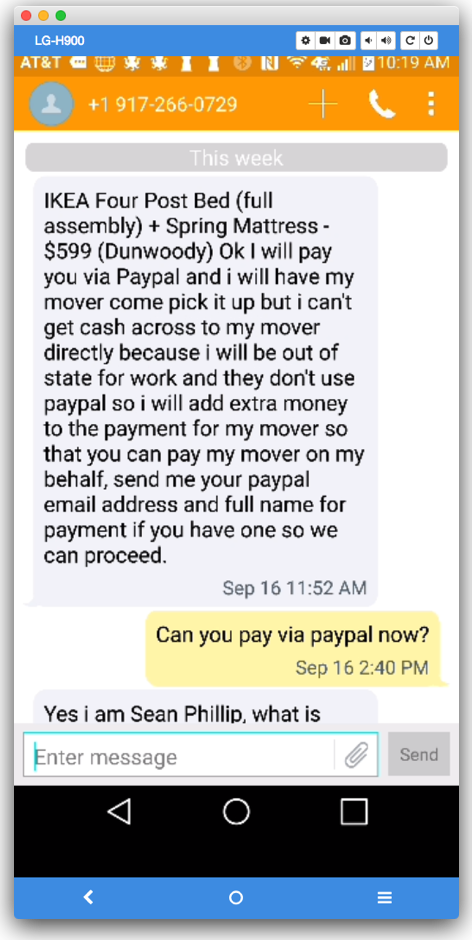

Moments later, I began to receive these text messages:

Let’s look at the first one:

That seemed legit. Sean Phillip gave me his name and said he was ready to pay with PayPal immediately.

How to Lose Money Using PayPal

I looked into the issues doing business with a stranger using PayPal. Here’s what I found:

When we enter into a transaction like this, PayPal takes the money ($599 + movers expenses) and puts that money in “escrow”. Escrow is just an account that holds the money until PayPal is convinced that both parties upheld their part of the deal.

The buyer puts their money in the escrow account. The seller sees the money and then is responsible for shipping the furniture to the buyer.

Looks simple and safe. But, looks can be deceiving…

PayPal will only deem the furniture shipped if the seller ships the furniture and gets a tracking number from UPS/Fedex. However, that will cost at least $300; possibly thousands, depending on the amount of furniture to ship.

Since the seller cannot get any money until the buyer receives the furniture that won’t happen. So, the buyer will claim to have his movers pickup the furniture, which won’t happen either. Remember, this is a scam and the buyer is really only after the seller’s money.

Time goes by and the seller gets desperate; he’s told other prospective buyers that the furniture is already SOLD.

The buyer says he’ll send a check and by this time, the seller is motivated to accept it.

The Scammers’ Angle

The scammers’ angle is to get the central banking system involved because the banking system is flawed and the scammers can use those flaws to get the seller’s money.

Your bank will never lose (their) money, but they will charge you when you lose your money.

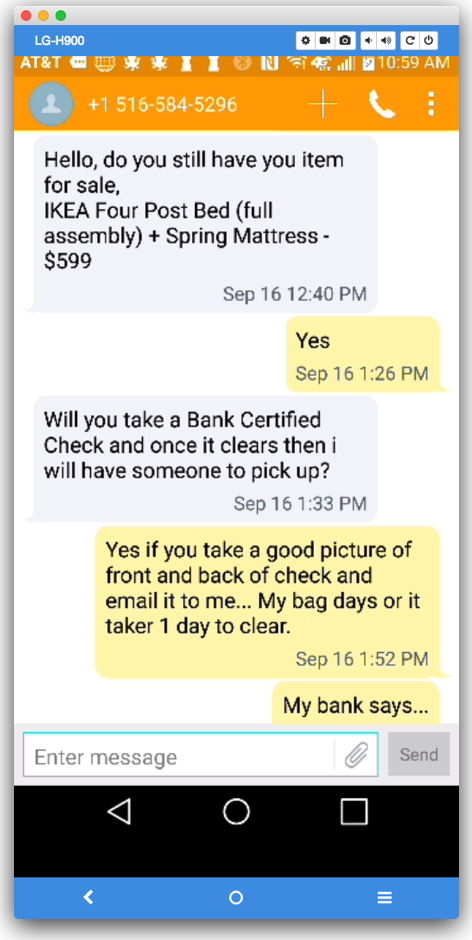

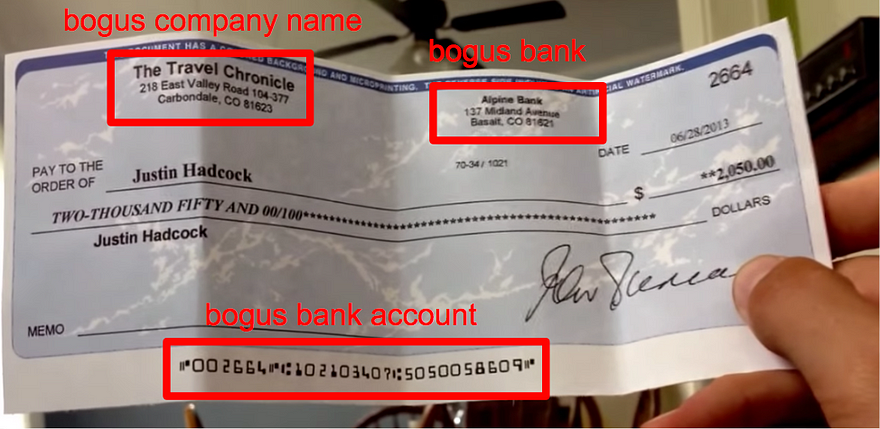

The Check Scam

It starts when the scammer gets you to agree to take a check.

Here’s how they do it:

Seller agrees to accept a check.

Buyer sends mover to pickup the furniture.

3. Seller receives a check for more than the cost “to cover moving expenses”.

4. Seller pays movers with their money $2,050 (to ship his furniture to a bogus person at a bogus address).

5. Seller sends extra $1,550 (the difference between amount of bogus check amount and how much the movers actually cost) to the buyer via Western Union.

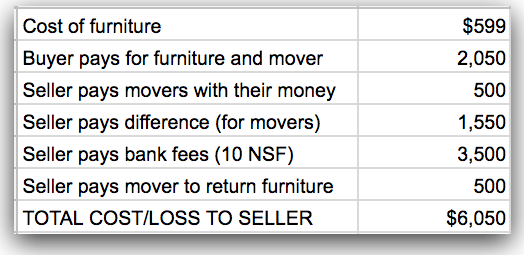

Where The Money Goes

All the amounts below could be real (and happen to you), except for the $2,050 (bogus) check from the buyer:

The buyer (scammer) makes $1,550.

The seller loses $6,050 (but still has his $599 furniture).

Your bank makes $3,500

The buyer does have some risk of getting caught, the mover makes a profit but has to work for it. Your bank makes out like a bandit and you’re left paying for it all.

Your bank will never lose (their) money, but they will charge you when you lose your money.

When the check clears and the seller sees the $599 credited to his bank account, he writes other checks assuming the balance that the bank claims is accurate is actually correct.

In this example, the seller’s bank account balance was just over $0.00 before the $599 clears. Suppose the seller trusts the bank’s report of his balance and makes 10 small purchases that subsequently all bounce. (Many banks give you immediate access to $200 from any check.)

The bank then charges the seller $35 for each of the 10 bounced checks ($3,500).

Suppose your (the seller) didn’t write any additional checks and have no NSF fees, you’ll still have to pay the movers $1,000 and you’ll still loose the $1,550 you paid the scammer. Plus, there will be a bank fee for “processing” a returned check. Also, this is not the only scenario where scammers (and banks) take advantage of sellers.

The Cost of the Middleman

None of this loss of money would happen if you, the seller, accept cash or cryptocurrency only. If you think that getting your bank involved in your transaction protects you, think again.

How bankers do it…

Bankers do it for a fee.

Bankers do it risk-free.

Bankers do it with glee.

The Real Cost

Let’s not forget your time lost communicating with the scammers, movers, PayPal and your bank representatives. Also, any NSFs may result in a negative impact to your credit rating, which will drive up all sorts of costs, including but not limited to new mortgage rates, insurance, college loans, ability to rent, etc. That could mean loss of opportunity and much more than your current $6,050 loss.

Our Banking System Enables Scammers

First, we must understand that banks are not in business to help consumers.

Banks exist to make a profit. Banks are like a monopoly that makes the rules, controls the rules and then decides how much to charge you when they can catch you breaking any of the rules (that are stacked against you).

Banks use deception to lure consumers into thinking that the account balances and transactions are real. Clearly, the only things you can count on are banks fees.

Dolor Emptor

I wonder how many check scams are instigated by the banking system. After all, who is guaranteed to profit (and never get caught)?

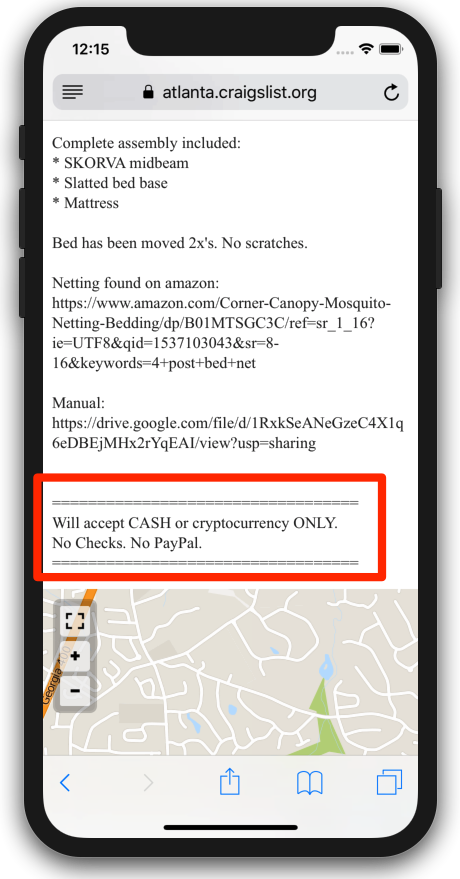

Craigslist — Will accept Cryptocurrency!

I added the following to my ad to reduce contact from scammers:

==================================

Will accept CASH or cryptocurrency ONLY.

No Checks. No PayPal.

==================================

Today’s reality is that only 5% of people use cryptocurrency. So, accepting cash is still a necessity on craigslist.

Lessons Learned

Do not trust your bank account balance

Do not accept checks from a stranger

Do not accept PayPal payments from a stranger

Do accept cash or cryptocurrency from anyone

Do use common sense

Who would pay over a $1,000 dollars to move furniture that’s only worth $599?

Go to the effort of tracking all of your deposits and credits separately from your bank’s account records. (Do not trust your bank’s version of your account balance.)

Other Financial Risks Sellers Face

If you accept PayPal or credit cards (Visa, MasterCard, etc.) you have to be concerned with charge backs. That’s when the buyer claims that what you sold them is not what they expected. Buyers are protected, not the seller.

If you are dealing with a dishonest buyer, they’ll do or claim anything to get money and possibly return damaged merchandise, if you’re lucky. Your credit will be affected and your rates will go up and you might get dropped from your bank’s merchant program.

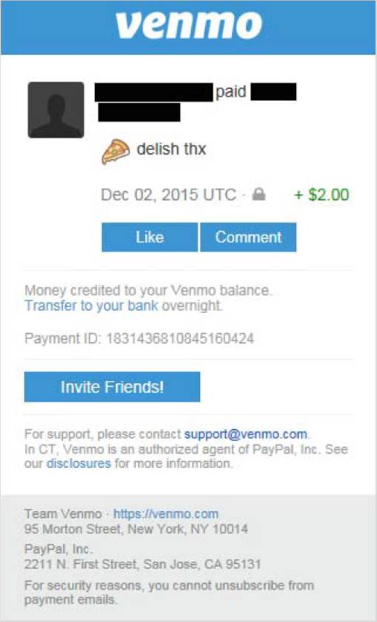

What about Venmo?

You’re not safe accepting Venmo payments either.

Read Venmo’s User agreement closely:

“Business, commercial, or merchant transactions may not be conducted using personal accounts.”

Scammers are exploiting a flaw in the Venmo system.

There is a gap between when you see the “Money credited to your Venmo balance. Cash out to your bank overnight.” and when you actually receive your money.

So, if you (the seller) read that “Money credited to your Venmo balance.” and think it’s safe to give your goods/services to the buyer, but if that buyer is a scammer, the next notification you’ll get will say ‘Your transaction has been reversed. ” and you’ll have no recourse.

The Flaw

Our banking system, PayPal and Venmo share the same flaw. It’s based on the business need to meet end user/buyer expectations. Buyers want to get what they want when they pay for it.

Using checks and Venmo only works if the buyer is honest.

The reality is that neither the current banking system or Venmo (or PayPal for that matter) can actually handle immediate transactions.

Their systems require “processing” time.

Scammers find ways to exploit the gap in what we think happens and what actually happens.

The main difference is that when we use banks, we not only lose money, but we also get penalized with banking fees.

The Solution

We need a system of exchange that can either eliminate that “processing” gap or make it so small and/or so secure that even the most wily scammer is unable to game it.

Each state has its own money transmitter regulations. Most states are way behind the times in regards to cryptocurrency. States regulations vary wildly.

Q: Why should you care?

A: Because you can be arrested and charged with financial crimes for unlicensed transmission of Bitcoin or other cryptocurrencies.

Definitions

FinTech: Financial Technology allowing commercial banks to use online delivery systems to market their banking products and services to customers outside the banks’ geographic branch footprints.

FinCEN: The Financial Crimes Enforcement Network of the United States Department of Treasury.

Money Transmitter: Any business performing money transmission. (Exact definition varies by state.)

Money Transfer Service: Any business entity that provides money transfer services or payment instruments. Money Transmitters in the US are part of a larger group of entities called money service businesses (MSBs).

Federal Crime

Transmitting money without a license is outlawed in 48 states and the District of Columbia, and it was made a federal offense under the Patriot Act in 2001. This is mostly a consumer protection policy meant to make sure people’s money isn’t transmitted by fraudulently.

Money transmitters must register with the proper state agency and may need to register with the FinCEN. They are also required to implement specific anti-money laundering policies and file regular reports.

Money transmission is a broad term, but its legal definition is much more narrow. Cryptocurrency investors are not automatically subject to state and federal regulation simply because they send Bitcoin or other virtual currencies from one person to another. Rather, a money transmitter must be licensed if it exchanges virtual currency for real currency, other virtual currency, or other value.

Who Needs to Register as a Money Transmitter?

Any business that conducts more than $1,000 in business in any category of activity listed below:

Check Cashing

Money Orders

Currency Exchanges

Money Transfer Services

Traveler’s Checks

What’s the Best State For Cryptocurrency Entrepreneurs to do Business?

Very few states have explicitly amended legislation to address cryptocurrency. Most states have not dealt with the issue and could put you in legal jeopardy.

In my next article, I’ll attempt to rank the states for cryptocurrency friendliness.

Are Your Wages Money?

Do you consider the wages/salary your employer pays you to be “money”?

In the United States, employees could be paid in cryptocurrency. However, it would be difficult for the employer to comply with U.S. tax laws.

Several U.S. based-companies are paying their international workers in Bitcoin. About 200 companies are using a service called Bitwage, a Bitcoin payroll company that allows W-9 and 1099 workers to receive payments in Bitcoin, according to Bloomberg Law.

What do You Think?

Economists define money as something that serves as a medium of exchange, a unit of accounting, and a store of value. Money is a medium of exchange when everyone agrees to accept it in making transactions. Does everyone accept it now?

When Bitcoin began, it was not accepted. Now, it’s gradually becoming more and more accepted.

Gaining Understanding and Confidence

What is money?

What are digital currencies?

Are cryptocurrencies money?

How do they work?

Find out the answers to these questions an more.

Day 1 of the Cryptocurrencies Developers Class is all about money (what it is, its history and relationship to digital currencies) and would serve as a good educational resource for those in finance and insurance professions.

The rest of the course is about how to leverage our understanding of money and blockchain technologies to build our own cryptocurrency.

Join me in class where we’ll:

Distill facts from fiction

Provide pertinent resources on a guided journey of learning

Provide well structured lab assignments

Provide starter projects (and completed solutions)

Provide insightful visual presentations

Provide a Certificate of Completion to attendees that finish the assignments

… and that’s just the 1st half of the course. In the 2nd half we cover the Ethereum blockchain.

I have condensed this class into an Immersive one week Master Class in Atlanta, GA.

The class location is TBD but will not be far from the airport.

I’m working on getting a package, discounted hotel deal for out-of-town attendees.

Challenge:

Explain how a central bank prints money in 20 words or less.

The

Answer

At

first, I was fooled by this trick question.

As

it ends up, the central bank creates money, but it’s the treasury

department that actually prints the money.

The

Explanation

The

Central Bank creates money when it converts debt to cash or credit.

The

debt is comprised of Treasury bills, bonds, notes and TIPS.

Cash

includes bank accounts and marketable securities. Cash can also refer

to checks or any other form of currency that is easily accessible and

can be quickly turned into physical cash (paper money or coins).

It’s

a common misconception that the Central Bank prints money. However

the Treasury Department is actually the entity responsible for

printing paper currency and minting coins; the Treasury oversees the

Bureau of Engraving and Printing and the U.S. Mint.

When

we examine the US Money Supply context diagram below, we see that

there is a big difference between the actual money in circulation

(shown in green $) and how much money people perceive is in

circulation (shown in red):

How

Money is Created in the US

Fractional

Lending

The

magic that creates the excessive supply of money is called fractional

lending.

Banks

are only required to keep a small percentage the cash depositors give

them on hand available for withdrawal. When an individual or business

deposits $100, the bank $90 and only keep 10% of the deposit, aka

“reserves” on hand. This reserve requirement is set by the

Federal Reserve and is one of the Fed's tools to implement monetary

policy. Increasing the reserve requirement takes money out of the

economy, while a decrease in the reserve requirement puts money into

the economy.

This

process continues many times thereby putting more and more perceived

money into circulation. For example, say Alice deposits $100

into Bank A. Bank A turns around and lends out $90 to Bob. Bob puts

his $90 into Bank B and Bank B turns around and lends $81 to Cindy,

etc.

Treasury

and Federal Reserve

The

U.S. government has a vested interest in the health and welfare of

the country's economy. The Department of the Treasury works hand in

hand with the Federal Reserve to maintain economic stability.

Central

bank mandate: To keep our money valuable and our financial

system healthy.

The

Department of the Treasury and Federal Reserve work together to

maintain a stable U.S. economy. The Federal Reserve serves as the

government's banker, processing transactions, e.g., accepting

electronic payments for Social Security taxes, issuing payroll checks

to government employees and clearing checks for tax payments and

other government receivables.

The

Federal Reserve and the Department of the Treasury also work together

to borrow money when the government needs to raise cash. The Federal

Reserve issues U.S. Treasury securities and conducts Treasury

securities auctions, selling these securities on behalf of the

Department of the Treasury. Examples of Treasury securities include:

Treasury Bonds

Treasury Bills

Treasury Notes

Treasury Inflation-Protected Securities (TIPS)

Debt

The

U.S. Congress creates the U.S. Federal Budget and grants itself

permission to borrow money. The borrowing is accomplished by the U.S.

Department of Treasury issue debt contracts (Treasury Bonds and

Notes) Example: “We agree to pay the bearer $1,000 sixty days from

today. The Central Bank buys a lot of them.

A

treasury bill is a monetary policy instrument through which

government raise funds for short term requirements and commercial

banks invest their short term surpluses by buying these bills from

government.

Treasury

Inflation-Protected Securities (TIPS) provides protection against

inflation. The principal of a TIPS increases with inflation and

decreases with deflation, as measured by the Consumer Price Index.

When a TIPS matures, you are paid the adjusted principal or original

principal, whichever is greater.

(Un)Printing

Money

The

Federal Reserve has 12 regional banks that supervise commercial banks

in local areas. These regional federal banks are responsible for

meeting the physical currency needs of local banks, providing cash

and taking excess cash. They also take currency out of circulation

when it is deemed to be damaged, counterfeit or just too old. They

order newly printed bills and coins to replace discarded notes and

coins.

Gaining Understanding and Confidence

It's easy to get tripped up with questions about how the US monetary system works.

Throw cryptocurrencies into the equation and it can get down right confusing.

I grew up with a mom that was intrigued with US economy, gold, currency and investments.

I guess that's why cryptocurrency (and blockchain technology) is so interesting to me.

I get to combine the rhetoric that I heard in my formative years with my professional years.

So interested that I studied, developed software and a training course to help others "get it".